VIX options showed heightened activity in the November 19, 2025, $32 call options. Total daily volume reached 11,533 contracts (at the time of this trade). Compared to an open interest of just 2,474, this produces a strong V/OI ratio of 4.7. This indicates that most of today’s trades were newly opened positions rather than closing existing ones.

The contracts traded at $0.99 each, bringing the total premium outlay to approximately $1.1 million. With the VIX spot trading around 19.62 at the time of the trade, these calls represent a volatility bet that the index could see a sharp move over the next couple of months. The sheer size and fresh positioning suggest institutional traders may be hedging against or speculating on volatility of the overall market through VIX options.

(adsbygoogle = window.adsbygoogle || []).push({});Volume and Open Interest Data

The VIX options historical trading data for November 19, 2025, $32 calls experienced a major surge in trading activity on September 24th. 13,748 contracts traded compared to an open interest of only 2,474, reflecting a very high V/OI ratio of 5.6. This suggests that the majority of contracts were newly opened positions rather than closing trades.

Open interest has been slowly climbing but remains far below the sudden spike in volume, signaling fresh speculative or hedging demand. At the same time, the contract price rose to $1.03 with implied volatility climbing above 154%. This reinforces the expectation of elevated volatility ahead. This unusual activity points to significant positioning in VIX options, potentially in anticipation of increased market turbulence.

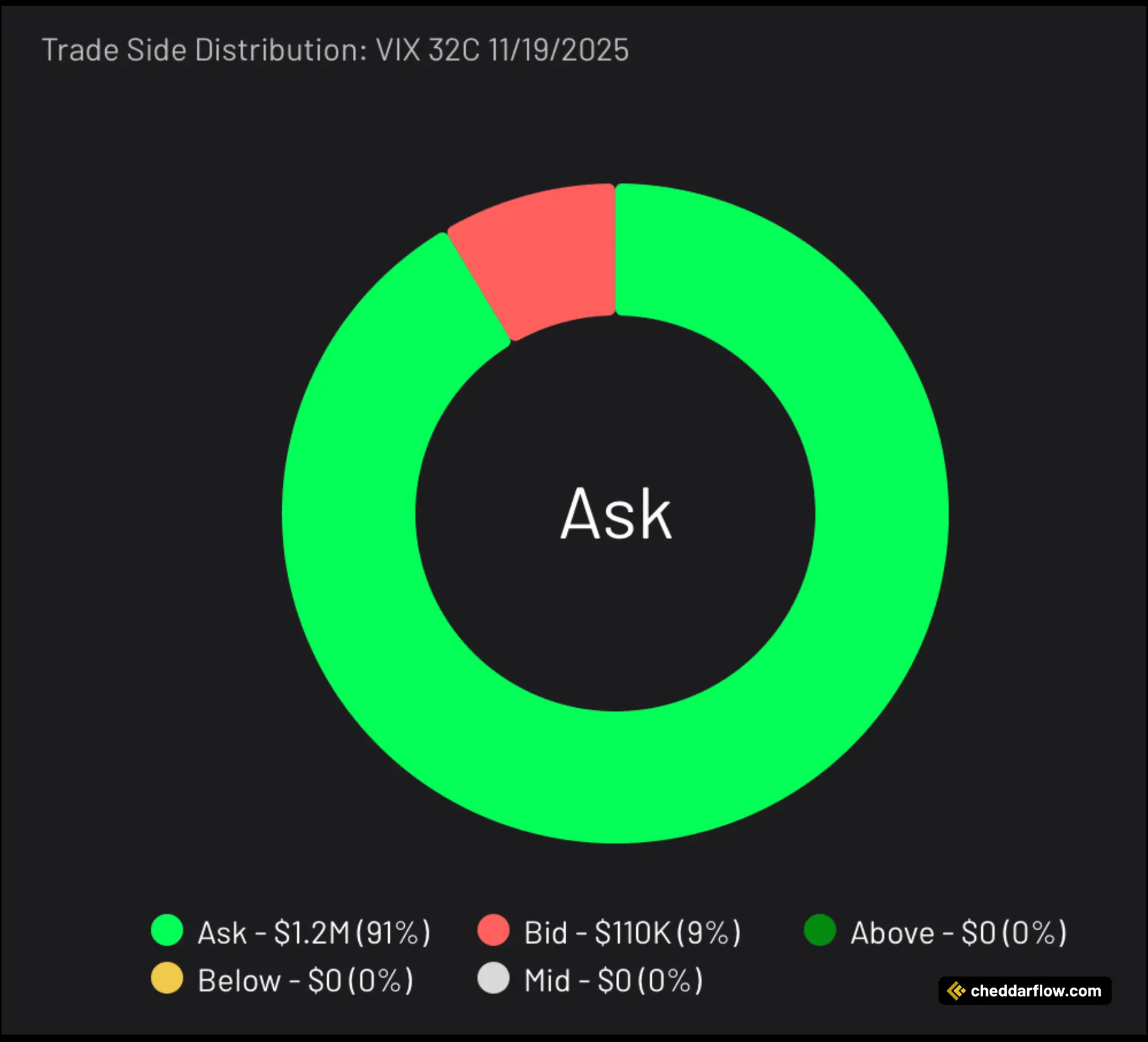

(adsbygoogle = window.adsbygoogle || []).push({});Trade Side Distribution

The trade side distribution for the VIX options November 19, 2025, $32 calls shows a strong buy-side bias. 91% of the activity ($1.2M in premium) executed on the ask side, indicating dominating buying interest. Only 9% ($110K) took place on the bid side. Meanwhile, no trades occurred at the mid, above, or below market levels.

This drastic skew toward ask-side buying highlights that traders were willing to pay up to secure positions. This signals institutional players may be positioning for a significant move in VIX options.

More Notable Options Trades Observed

VIX options also revealed unusual activity in the October 22, 2025, $23 calls The contract saw a massive order flow, with 20,000 contracts traded at a price of $1.00, totaling a $2 million premium outlay. This trade occurred with the VIX spot at 18.22, making it a sizable out-of-the-money volatility bet.

The day’s volume of 20,092 contracts is nearly identical to the block size, suggesting a single large order dominated activity. While open interest is already high at 145,971 contracts, the scale of this trade still stands out as significant institutional positioning. Given the mid-market execution, this may represent a mix of aggressive buying and selling. However, the sheer size highlights strong speculative or hedging interest ahead of the October expiration.

What’s Happening with the VIX

The VIX, often referred to as the “fear index,” measures the market’s expectation of volatility in the S&P 500 over the next 30 days by analyzing option prices. Typically, the VIX moves inversely to the S&P 500. When the S&P 500 declines—often due to increased uncertainty or fear in the markets—the demand for options rises.

This causes implied volatility (and thus the VIX) to spike higher. This happens because investors seek protection against further declines, bidding up option prices as they hedge their positions. Conversely, when the S&P 500 is rising and market sentiment is calm, the VIX generally falls, reflecting lower expected volatility ahead.

(adsbygoogle = window.adsbygoogle || []).push({});About the VIX

The CBOE Volatility Index (VIX) is Wall Street’s widely watched “fear gauge.” It represents the option market’s consensus view of how volatile the S&P 500 will be over the next 30 calendar days. It does so by aggregating real-time prices of a broad strip of near-term out-of-the-money S&P 500 index calls and puts. When those option premiums rise—signaling traders are willing to pay more for protection against, or participation in, large index moves—the VIX climbs. Likewise, when premiums fall, the VIX declines.

Importantly, the VIX is a forward-looking, implied-volatility measure, not a historical one. It is expressed in annualized percentage terms. So, a VIX reading of 20 implies roughly ±1.25 % daily moves in the S&P 500 over the coming month under a log-normal assumption. Investors use it both as a barometer of market sentiment and as a tradable instrument for hedging or speculating on near-term equity-market turbulence.

Want to see more of these trades? Try out Cheddar Flow free for 7 days. Learn More

Disclaimer: Options trading involves significant risk and is not suitable for all investors. You may lose the entire investment, and certain strategies may result in losses exceeding the initial amount invested. Past performance does not guarantee future results. This content is for informational purposes only and should not be considered investment advice. Always consult a financial or tax advisor before making investment decisions.