In the day leading up to the Federal Open Market Committee’s (FOMC) interest rate announcement, there was a marked uptick in put option activity across major U.S. indices, particularly SPY and QQQ. This surge in flow reflects heightened caution among traders, many of whom sought protection against potential downside volatility stemming from the central bank’s policy decision.

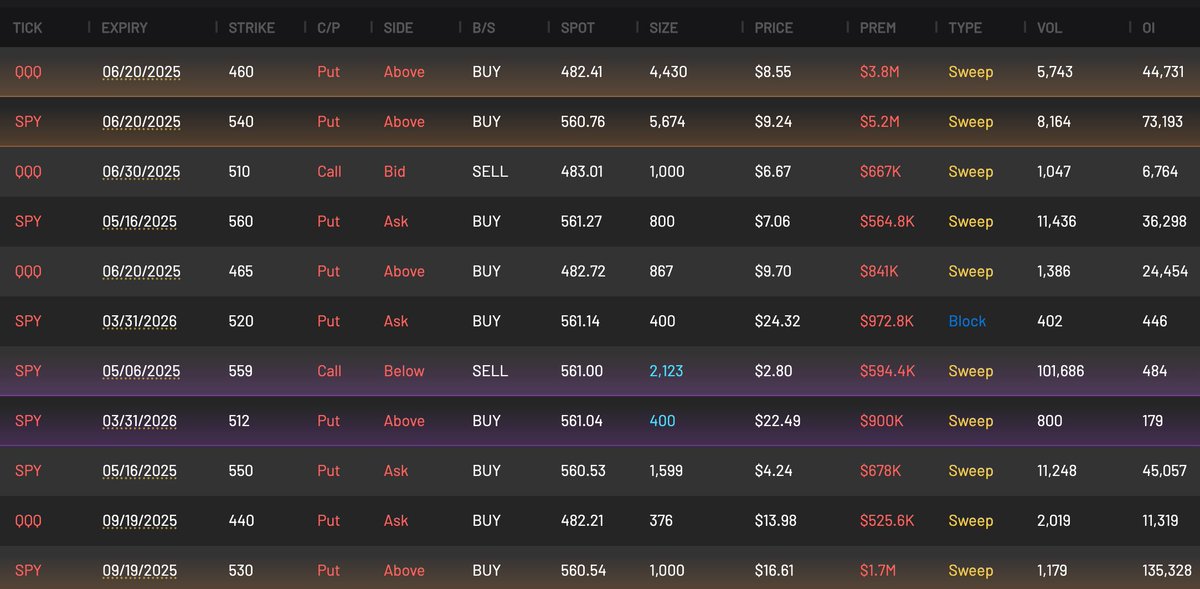

Within SPY, the most notable concentration of activity occurred in the May 6th expiry, the shortest-dated option available. One specific trade stood out: a massive volume of 101,686 contracts on the 559 strike call compared to an open interest of just 484 contracts. This volume-to-open-interest ratio of over 200:1 strongly suggests the establishment of new positions, likely driven by near-term speculative or hedging motives.

In addition to sheer size, the nature of the order flow was equally telling. The majority of these trades were executed as sweeps—a tactic used when urgency is paramount and traders are willing to pay through the offer to ensure immediate execution across multiple exchanges. This reinforces the notion that participants were aggressively seeking exposure ahead of the Fed’s decision, signaling elevated risk perceptions.

Furthermore, in the 540 put strike for SPY, traders committed a total of $5.2 million in premium, underscoring the scale of bearish positioning or hedging taking place.

Overall, the data suggests a tactical rush into downside protection, reflecting a market bracing for volatility as the Fed signals its monetary policy trajectory. Whether these positions were purely protective or speculative remains to be seen, but the urgency and size of the flows clearly highlight the significance of this week’s FOMC event in shaping near-term sentiment.